Risk Factors

The Group is committed to ERM*1 as the management platform for promoting its Mid-term Business Plan. Specifically, we will be constantly aware of the relationship between “risk,” “capital” and “profit,” and by realizing “capital adequacy” and “high profitability” in relation to risk, we will strive to achieve sustainable growth of corporate value.

-

*1Enterprise Risk Management

The risks surrounding the Tokio Marine Group are becoming more diversified and complex due to our global expansion and changes in the business environment. In today’s uncertain and rapidly changing political, economic, and social climate, we must proactively anticipate the emergence of new risks and their warning signs and take appropriate action. From this perspective, we are not limited to conventional risk management aimed at risk mitigation and avoidance, but are comprehensively assessing risks through both qualitative and quantitative approaches, including risks not previously recognized.

In addition, we are continuing our efforts to further strengthen the ERM framework. For instance, we are enhancing risk assessments to include risks that are difficult to quantify, such as cyber risks, and improving natural catastrophe risk management, including through reviews of our reinsurance schemes.

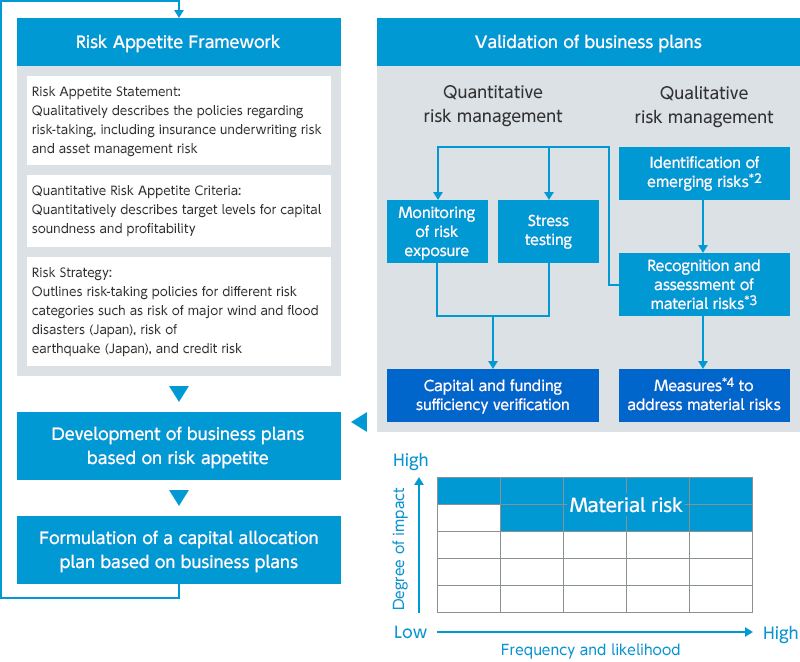

ERM Cycle

-

*2Emerging risks are new risks that arise due to changes in the environment or other factors, encompassing those that were not traditionally recognized as risks and those that have increased markedly in severity.

-

*3Material risks refer to risks that could have a substantial impact on financial soundness, business continuity, and other critical aspects. Specifically, we focus on emerging risks as well as material risks from the previous business year within the Group. We assess the impact (evaluating economic, business continuity, and reputational impacts) and consider the frequency and likelihood to identify the most significant factors. We specify these risks using the following 5×5 matrix.

-

*4For material risks, we formulate response measures (Plan), implement these measures (Do), assess the outcomes (Check), and make improvements (Act).

(1) Qualitative Risk Management

In qualitative risk management, all risks, including risks that emerge due to changes in the environment and risks not previously recognized, are identified and reported to management, while risks to the Group are discussed at the management level as needed.

Risks identified in this manner are evaluated not only in terms of the economic loss or frequency of occurrence but also in terms of business continuity and reputation. Risks that have a large impact on the financial soundness and business continuity of the Group or of individual Group companies are identified as “material risks.” For identified material risks, we assess the sufficiency of capital through the quantitative risk management process described in the subsequent pages, formulate control measures before the risks emerge and countermeasures*5 to be taken if the risks do emerge, and conduct PDCA management.

In addition, while we have been implementing such risk management practices, in light of the information leakage incident that occurred at TMNF, we have strengthened measures addressing “legal and regulatory compliance/conduct risk,” one of our key risks, and newly included “leakage of critical information” to our risk response measures.

-

*5Pre-event risk controls include monitoring and aggregated risk management that consider market conditions and regulatory trends. Post-event measures include preparing manuals (including business continuity plans) and conducting emergency drills.

Detection of Emerging Risks and the Process of Identifying Material Risks

![[Emerging Risks] New risks that emerge due to changes in the environment or other factors, and that have not been previously recognized as risks, or risks that have increased markedly in severity. Potential emerging risks: Emerging risks for major Group companies. New emerging risks identified by the CRO or risk management department. Emerging risks identified in the previous fiscal year. Risk information from external sources. 1 Screening → Emerging risks → [Material Risks] Risks that have a significant impact on financial soundness, business continuity, etc. Potential material risks: Material risks of the Group in the previous year. High-impact risks among the emerging risks. 2 Identification by matrix evaluation → Material risks → PDCA for material risks](/en/ir/financial/images/img_risk_02.png)

Examples of emerging risks

| Emerging risks | Examples of responses |

|---|---|

|

|

|

|

|

|

|

|

|

|

Material risks for fiscal 2025

| Material risks | Examples of responses |

|---|---|

|

|

|

etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(2) Quantitative Risk Management

In quantitative risk management, the Company quantifies potential risks and conducts stress tests using risk models based on the latest knowledge available, verifying from multiple perspectives that its capital is sufficient relative to the risks it holds, with the aim of maintaining its credit ratings and preventing bankruptcy.

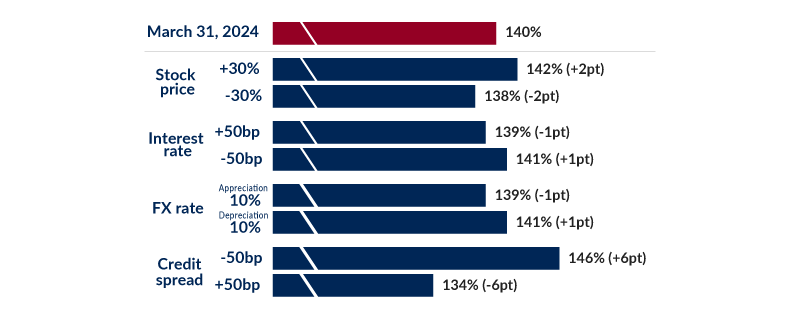

Specifically, the Company quantitatively evaluates risk using Value at Risk (VaR) at a 99.95% confidence level and verifies capital adequacy through the Economic Solvency Ratio (ESR), calculated by dividing net asset value*6 by risk capital. Our capital policy is determined comprehensively considering business investment opportunities and future market outlooks, among other aspects. A 99.95% VaR represents the potential loss from a risk event expected to occur once every 2,000 years, which corresponds to an AA credit rating.

The target range for the Group’s ESR is 100%‒140%, and as of March 31, 2025, the Group’s ESR was 149%*7, confirming that capital levels are sufficient.

For certain key risks namely, economic and financial crises, major earthquakes, and pandemics we conduct stress tests on capital adequacy and liquidity based on scenarios assuming extremely large economic losses, as well as scenarios in which multiple material risks occur simultaneously. Stress tests on liquidity are also conducted for major wind and flood disasters. In all cases, we have confirmed that no issues exist.

-

*6Calculated by adding the value of catastrophe loss reserves, deducting for goodwill, and making other adjustments to consolidated net assets on a financial accounting basis

-

*7ESR after executing share repurchases of 220 billion yen in treasury stock is 143%.

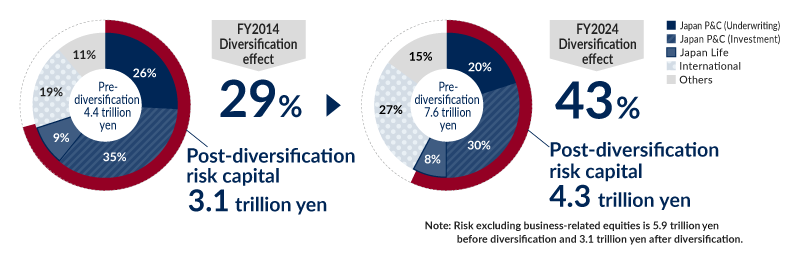

Risk Composition and Diversification Effects

ESR Sensitivity