CFO Letter

We have consistently achieved “top-tier EPS growth” through sustained strong profit expansion in both insurance underwriting and asset management, while managing volatility. In addition, with a clear aspiration to raise ROE to the level of global peers through disciplined capital policy, we have been steadily executing this policy. As Group CFO, I am deeply involved in management decision-making, particularly from the perspective of capital policy, to enhance the Company’s corporate value.

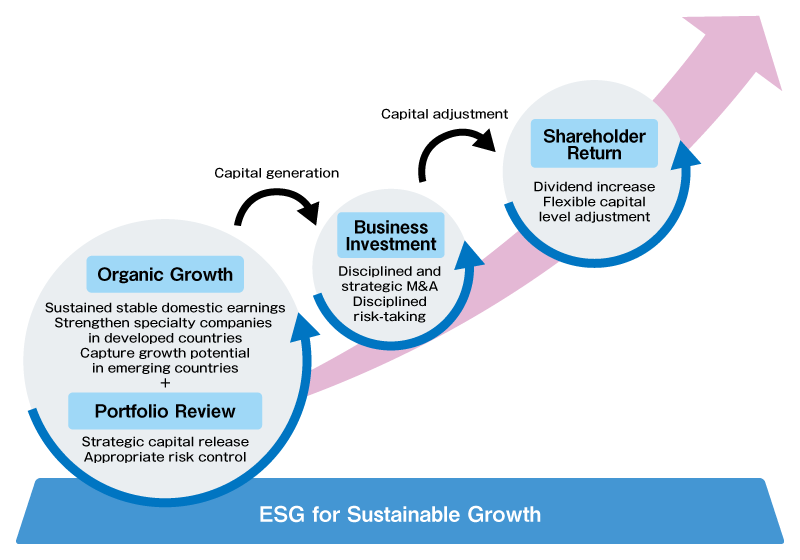

In particular, the capital circulation cycle that we emphasize is implemented through a three-pronged approach. First, based on internal growth and strategic review of the portfolio, we generate capital and funds. Second, the capital and funds generated are allocated to strong business investments. Third, if suitable investment opportunities are not available, capital is returned to shareholders. By continuously executing this cycle, we aim to enhance ROE. This approach goes beyond simply pursuing capital efficiency; it provides a foundation for achieving both prudent risk-taking and medium- to long-term profit growth. In the following sections, I will provide an explanation of our capital policy and its outlook.

Tokio Marine Group’s capital circulation cycle

Organic Growth

First, regarding organic growth, we are not pursuing a so-called shrink-to-balance approach. The primary driver of ROE improvement is expanding the numerator—that is, achieving top-tier EPS growth based on organic growth.

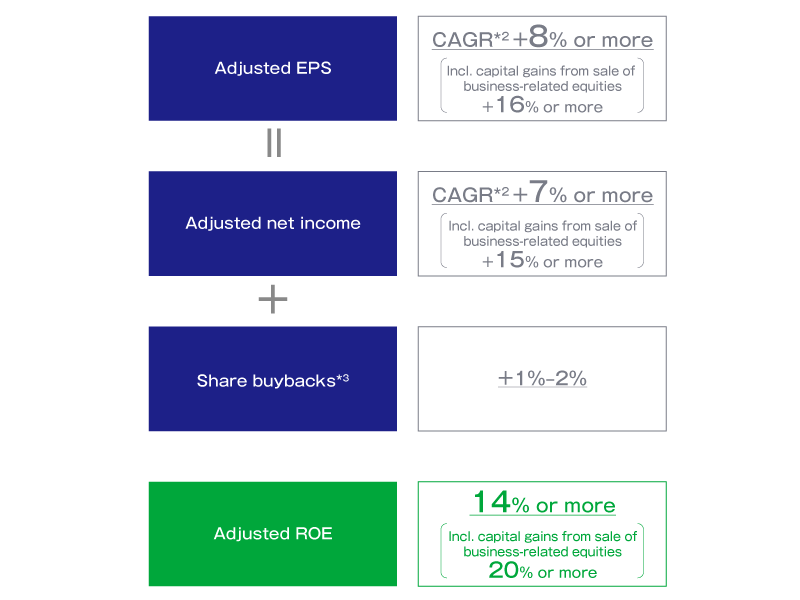

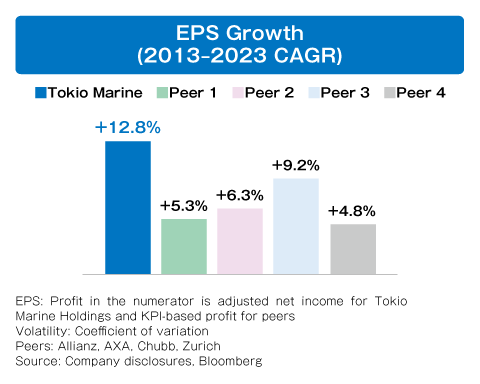

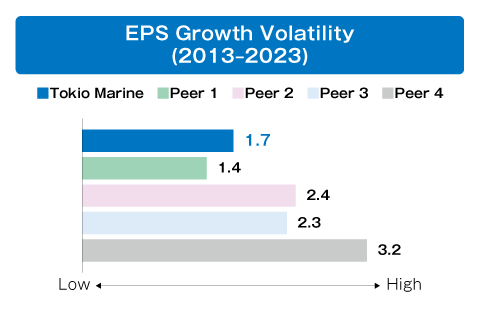

In fact, we have consistently achieved “top-tier EPS growth” through sustained strong profit expansion in both insurance underwriting and asset management, while managing volatility, achieving results that are comparable to—or even exceed—those of global peers. The EPS growth target in the Mid-Term Business Plan is set at a CAGR of 8% or more*1, which is expected to be achieved through profit growth of 7% or more and the impact of share buybacks of 1%‒2%.

Our portfolio is well-diversified across (i) stable revenue sources, such as the Japanese non-life insurance business; (ii) the broad and high-potential North American specialty sector; and (iii) emerging markets, including Brazil and Asia, with strong growth prospects. This diversification underpins the continuity and sustainability of EPS growth across the Group.

-

*1On a basis excluding gains from the sale of business-related equities.

Portfolio Review and Business Investment

We continuously review our business portfolio and allocate capital based on considerations such as which risks to take, to what extent, and whether the expected returns are sufficient. As Group CFO, I engage in ongoing discussions with the heads of each business to evaluate strategies that form the basis for capital allocation, supporting growth across the company and directing resources according to future growth expectations. Most recently, TMHCC has steadily captured opportunities in high-growth areas, acquiring GGEBS in July 2023 and Lasso in April 2025.

We pursue appropriate capital allocation by executing bolt-on M&A and growth investments (Entry), such as establishing a local subsidiary in Canada in 2022 where we anticipate country- or region-level growth, while divesting (Exit) local subsidiaries in Guam and Saudi Arabia where we judged that we are not the best owner. Regarding large-scale M&A deals, we recognize that current valuations are still relatively high, so we will remain patient while seizing opportunities in a timely manner with disciplined acquisition practices.

(Reference)

Entry strategy (Acquisitions & establishments)

-

The ROI*1 of our large-scale M&A is 21.2%, significantly exceeding our cost of capital (7%).

-

Small to medium-sized bolt-on M&As are being steadily executed.

Exit strategy (Divestitures & run-offs)

-

For our exit strategy, we evaluate the future potential of businesses in a forward-looking manner and execute divestments with discipline.

-

*1ROI is calculated using the simple sum of projected 2025 business-level profits as the numerator and the simple sum of acquisition amounts as the denominator.

(Reference)

Rate cycle and M&A opportunities

Current valuations in M&A remain elevated, reflecting the underwriting “rate cycle.” Specifically, during a “hard market”—when insurance demand exceeds available capacity—premium increases support organic growth, leading to higher valuations. Conversely, in a “soft market,” valuations tend to decline, making it easier to execute high-quality M&A deals at appropriate prices. We have consistently executed M&A with discipline while closely monitoring these market shifts. Even as we accelerate the sale of business-related equities and generate excess capital, we will not change the principles or discipline of our entry and exit strategies. Going forward, we will continue to steadily pursue growth investments that enhance Group-wide ROE, while seizing M&A opportunities in line with the rate cycle to further improve capital efficiency.

-

*2U.S. commercial market (Source: WTW, Commercial Lines Insurance Pricing Survey)

-

*3Aggregated global deals in the non-life insurance sector with project amounts of USD100 million or more announced between 2003 and 2024. (Source: Dealogic).

-

*4Dates refer to announcement dates.

Raising ROE to Global Peer Levels

Alongside EPS growth, we are committed to the market on another key KPI: raising ROE to global peer levels.

Our ROE for fiscal 2024 was 19.8%. On a basis excluding gains from the sale of business-related equities, which reflects our core insurance operations, ROE was 12.6%. Although these figures are among the top in Japan’s financial sector, we recognize that there remains a gap compared to global peers.

the main driver of our ROE improvement is the expansion of the numerator—that is, top-tier EPS growth based on organic growth. This is a goal that global peers are also striving to achieve (“0”on the chart below). In addition, we have two unique drivers for raising ROE that global peers do not have (“1” and “2”on the chart below).

The first is the transformation of the business portfolio (“1”on the chart below), in which surplus capital generated from the sale of business-related equities is reinvested into core businesses with higher Return on Risk (ROR).

Approximately 0.7 trillion yen of risk previously tied up in business-related equities can now be released. This represents a driver for ROE improvement that global peers do not have.

The second driver is the expansion of the solutions business, which we have positioned as a new pillar of our future growth strategy. This business primarily consists of the low-capital fee business, such as the disaster prevention and mitigation consulting provided by ID&E. Although our global peers already operate fee businesses at a considerable scale, we are only now beginning full-scale development in this area and this represents significant opportunity for ROE improvement (“2”on the chart below).

By fully leveraging these drivers, we will achieve our goal of raising ROE to the level of global peers.

Adjusted ROE*1, *2

-

*1Normalized natural catastrophes to an average annual level and excluding capital gains/losses in North America, etc. (for part of change from the initial plan). For the FY2024 calculation, the amount of the capital losses budget in North America has been revised from -USD265 million (before tax), which was the original plan for FY2024, to -USD440 million (before tax).

-

*2For peers, disclosed ROEs as their KPIs are adjusted to the tangible basis to align them with TMHD’s adjusted ROE (Source: Estimated by TMHD using company data).

Progress on Reducing Business-Related Equities and Transformation of the Business Portfolio

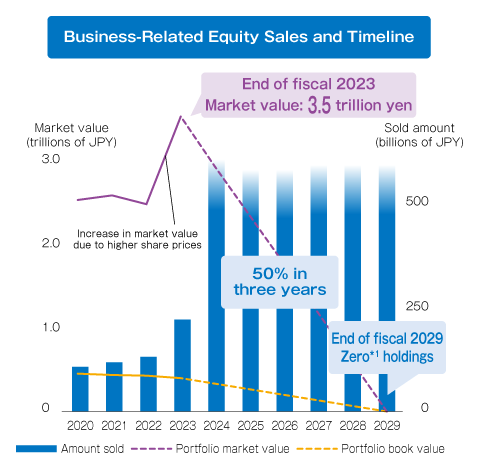

The steady execution of business-related equity sales forms the foundation for the first driver of ROE improvement: the transformation of the business portfolio. In May 2024, the Company announced its target of reducing business-related equities to zero by the end of fiscal 2029, with an interim milestone of halving the balance over the three years of the current Mid-Term Business Plan. In fiscal 2024, actual sales exceeded 900 billion yen versus the initial plan of 600 billion yen, and for fiscal 2025, 600 billion yen in sales are planned, reflecting an accelerated divestment pace.

On the other hand, unrealized gains on business-related equities are already included in capital, so their sale does not create new capital. A key challenge is how effectively the risk released through these sales can be deployed into growth-oriented, value-enhancing business investments. The effective way to deploy this risk—namely, a lever to raise the Company’s ROE—is the transformation of the business portfolio.

As shown in the chart below, ROE can be decomposed into Return on Risk (ROR) multiplied by the Economic Solvency Ratio (ESR), meaning that improving ROR directly drives ROE enhancement. Currently, the Group’s overall ROR stands at 17.9%, which can be further broken down into 20.4% for the core insurance business and 6.0% for holdings of business-related equities. From this perspective, it is evident that holding business-related equities acts as a drag on our ROR. By reallocating the risk released through these sales to core businesses with higher ROR, we can naturally increase overall ROR. Specifically, this could involve selectively increasing underwriting risk in North American operations, where we already have a strong business foundation, or expanding asset management. Through such new capital deployment into core businesses, we aim to raise ROE.

Sales of business-related equities

Reinvestment into higher-ROR businesses (Transformation of business portfolio)

-

*1Adjusted net assets are calculated as the average balance of consolidated net assets on a financial accounting basis, adjusted for catastrophe loss reserves, goodwill, etc. In contrast, net asset value (after deducting restricted capital) represents the end-of-period balance on an economic value basis, with assets and liabilities measured at market value. As the definitions differ, figures on each side of the equation do not match.

-

*2After distribution; after tax.

-

*3As of March 31, 2025.

Shareholder Return

We attach great importance to delivering shareholder returns consistent with sustainable profit growth, and our policy in this regard remains unchanged. Specifically, our approach is to position ordinary dividends as the foundation of shareholder returns, with the goal of steadily increasing the Dividend per Share (DPS) in line with profit growth. In practice, the basis for dividends is defined as the five-year average adjusted net income, which helps smooth volatility, and we set the ordinary dividend at 50% of that amount. In fiscal 2024, in addition to steady profit growth, we recorded significant gains from the sale of business-related equities, which lifted the five-year average adjusted net income—the basis for dividends—to a record-high level. As a result, DPS for fiscal 2025 is expected to mark the 14th consecutive year of increase, up 22% year on year to 210 yen.

With respect to share repurchases, we take a flexible approach, considering a comprehensive set of factors, including the level of our Economic Solvency Ratio (ESR), market conditions, opportunities for additional risk-taking, and a scale that would lift EPS growth by approximately 1%‒2%. For fiscal 2025, we plan total share repurchases of 220 billion yen, and in May, we approved the first-half execution of 110 billion yen.

Changes to KPI Definitions due to the IFRS Transition

We plan to transition to International Financial Reporting Standards (IFRS) at the end of fiscal 2025. The introduction of International Capital Standards (ICS) for Japanese insurers is also scheduled around the same time.

We plan to review the definitions of various KPIs, including profit metrics, and the approach to determining the dividend base. However, our policy of delivering DPS growth in a manner consistent with world-class EPS growth will remain unchanged. This will improve comparability with global peers. The new definitions, taking into account dialogue with the capital markets, are scheduled to be provided by the autumn of 2025 at the latest.

Enterprise Risk Management (ERM)

As an insurance company, we increase returns by taking risks in insurance underwriting and asset management as a key to our business. We have positioned Enterprise Risk Management (ERM) as the cornerstone of Group management. ERM takes into consideration our risk appetite, to what extent we undertake risks (risk boundaries), whether return on risk is sufficient, and whether risks are appropriately diversified. We have also established the ERM Committee to discuss ERM strategy. The committee assesses the growth potential and profitability of all businesses and the risks associated with each strategy in a forward-looking manner and formulates a capital allocation plan to optimize the risk portfolio from a Group-wide perspective. By doing so, we aim to achieve capital adequacy and high profitability relative to risk. This approach is intended to sustainably enhance our corporate value.