Risk Management

Risk Management System

To ensure financial soundness and appropriateness of business operations, Tokio Marine Group has identified the various risks surrounding it in an overall fashion and implements appropriate risk management corresponding to the nature, status, and other attributes of risks. The Company promotes the development and enhancement of the risk management system for the entire Group in accordance with the “Tokio Marine Group’s Basic Policies for Risk Management.” The Company also manages quantitative risks for the Group in order to maintain credit ratings and to forestall insolvency in accordance with the “Tokio Marine Group’s Basic Policies for Integrated Risk Management.”

Among various risks, the Company recognizes that insurance underwriting risks and investment risks must be managed as sources of earnings. The Company therefore controls these risks considering the balance between risk and return. The Company also identifies administrative risks, system risks, and other associated risks (such as operational risks) that arise from the Group’s business activities and strives to prevent the occurrence of or reduce these risks.

The Company indicates the Basic Policies for Risk Management, and, provides risk related instruction, guidance, monitoring, and other services to domestic and overseas Group companies. Group companies establish risk management policies in line with the policies of the Group and execute risk management independently.

Through the above measures, the Company executes proper risk management and ensures stable business operations of the entire Group.

Tokio Marine Group's Risk Management System

![Tokio Marine Holdings Audit & Supervisory Committiee Board of Directors Management Meeting GRSC / IER*/Investment Strategy discussions / Enterprise Risk Management (ERM) Committee Risk Management Department(Supervising Department)/Departments in charge [Insurance underwriting risks] [Investment Risks] Market risks / Credit risks / Real estate investment risks [Operational Risks, etc.] Liquidity risks / Administrative risks / System risks / Cybersecurity risks / Information leakage risks / Legal risks / Reputational risks / Accident/disaster/crime risks / Personnel and labor risks / Other risks ⇒ lndicatstruction of policies, instruction/guidance/monitoring [Group Companies] Domestic non-life insurance business / Domestic life insurance business / International insurance business / Solution business ⇒ Reporting](/en/company/governance/internal/images/img_risk_01.png)

-

*Investment Executive Roundtable

“Three Lines of Defense” for Risk Management

Our group has established “Three Lines of Defense” to strengthen our risk management system.

| Roles and Responsibilities | Department in charge | |

|---|---|---|

| First Line | Have primary responsibility for risk management in the assigned business. Based on the policies set by the second line, the first line will "identify and evaluate risks," "implement measures to reduce and manage risks," "monitor the risk situation," and "foster and promote a sound risk culture." | Business division |

| Second Line |

The second line will check and monitor the autonomous risk management of the first line and provide support as necessary. In addition, the second line will comprehensively grasp risks through both qualitative and quantitative approaches and implement integrated risk management. |

Risk Management Department Compliance Department |

| Third Line |

From an independent standpoint, the Third Line will evaluate the appropriateness and effectiveness of the processes implemented, the risk management and compliance systems established by the first and second lines and provides necessary advice and recommendations for correction. In addition, the third line will report the results of internal audits to management. |

Internal Audit Department |

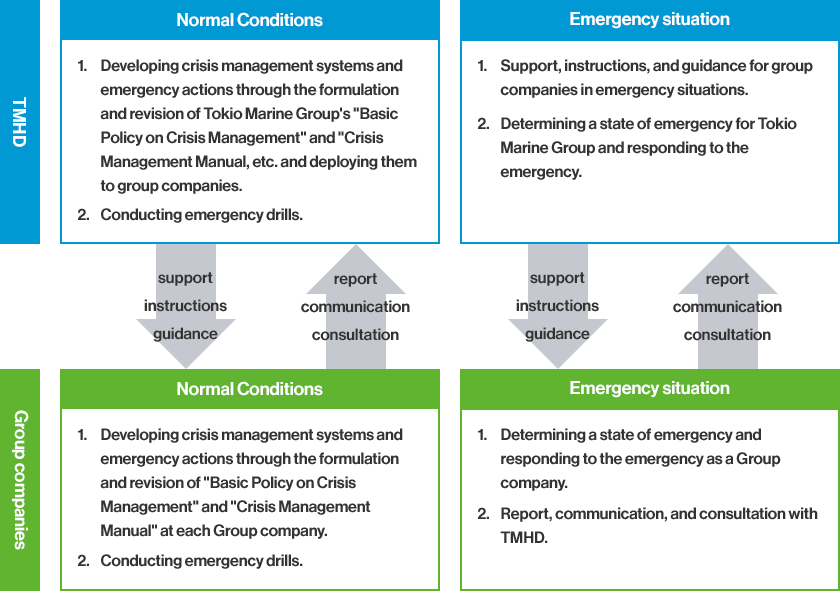

Crisis Management System

Even if appropriate qualitative risk management and quantitative risk management are conducted, it is difficult to fully control all risks, and there are also risks that cannot be avoided, such as natural disasters. Therefore, we have established a crisis management system, emergency actions, etc. to minimize economic losses and other impacts incurred in an emergency and immediately restore ordinary business operations.

In addition, we provide support, instructions and guidance to Group companies, and Group companies report, communicate and consult with us. In this way, Group companies also develop their crisis management systems and emergency actions during normal conditions, and respond quickly and appropriately for recovery and business continuity in the emergency situations.

Furthermore, we conduct emergency drills for natural catastrophes, cyberattacks, and other events that could become an emergency*, to improve our ability to respond to those situations.

-

*It refers to situations that have a significant impact on the relationship between each Group company and its stakeholders such as customers and agents, or situations that may cause significant disruption of the business operations in each Group company. Specifically, it assumes the occurrence of material risks such as natural disasters, pandemics, IT system failures, cyberattacks, leakage of personal/confidential information, significant violations of laws and regulations, business suspension orders from authorities and the occurrence of situations similar to those.

Tokio Marine Group’s Crisis Management System