How Lessons from the Great East Japan Earthquake Transformed Our Claims

- Insurance & Risk Insights

- Social Issues & Advancing Society

It has been 15 years since the Great East Japan Earthquake and 10 years since the Kumamoto Earthquake.

At the time, the front-line responders of Tokio Marine & Nichido Fire Insurance (TMNF) faced a stark barrier: how to deliver on their purpose to “be there for our customers and society in their times of need” during such large-scale disasters, and the ability to do so with existing systems.

Guided by the belief that claims shouldn’t be delayed under any circumstances, regardless the scale of the disaster, TMNF revamped their enterprise systems and reassessed their business processes. The result was a transformation from which came a payment system that functions even during large-scale disasters.

As a result of this transformation, the efficiency of claims processing has increased, leading to greater customer satisfaction. In this piece, we retrace TMNF’s journey, looking back on the challenges they faced and how the company evolved.

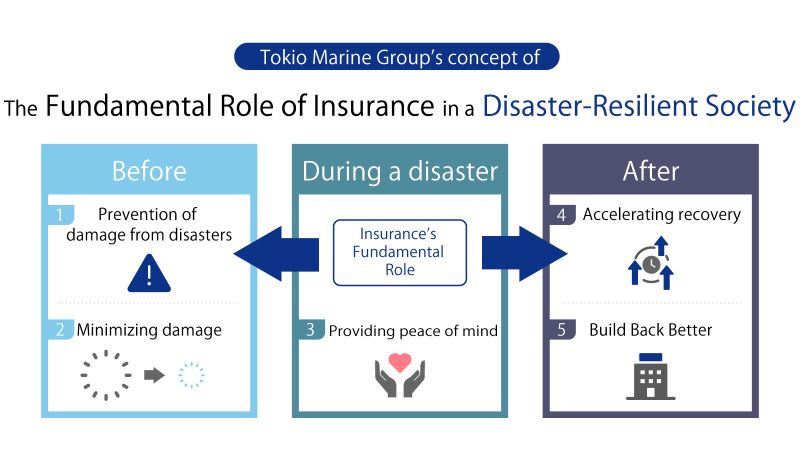

The Role of Claims Payment

Japan is one of the world’s most natural disaster-prone countries. Due in part to the effects of climate change, the damage caused by these events has been intensifying year by year.

Tokio Marine Group is there for customers and society across the disaster cycle, from preparedness and prevention to emergency response, and through to recovery and reconstruction. Central to this support is the prompt payment of claims. Timely, reliable payments support rebuilding lives and help bring forth a disaster-resilient society where everyone can live with peace of mind.

The Challenges Revealed by Large-Scale Disasters

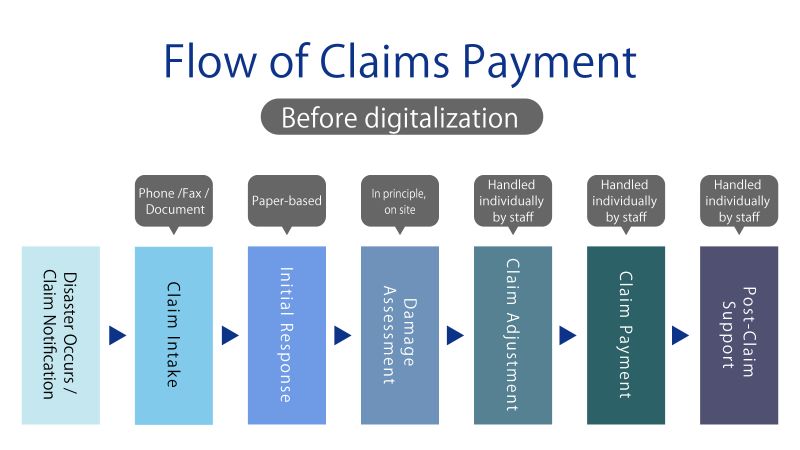

From an era of analog processes

One challenge at that time was how much customer service and internal processes still relied on telephone, fax, and paper-based operations.

Phone calls were the norm for claims intake from customers, and a lot of related information was shared with offices by fax. So whenever a large-scale disaster struck, phone lines were overwhelmed by the volume of calls. And since fax transmissions take time, information could not be shared in real time, causing delays in information flow for operations on the front lines.

Managing vast amounts of paper documents was also a major obstacle. Even to simply review past correspondence, staff had to dig through a mountain of documents to find the ones they needed. In addition, the process of re-entering the information from the received paper documents into the internal system created a redundant step, increasing the workload for the front lines.

The analog methods on which information management relied created physical limitations on how quickly we could respond. The consequence was long wait times for customers.

Evolution Through Digitalization

Driven by a sense of urgency, we resolved to undertake fundamental reforms that focused on revamping our enterprise systems and redesigning business processes. We rebuilt the entire process—from initial response to payment—from the ground up. Our aim was not merely to streamline processes. We needed to establish a robust claims payment system that would function regardless of the scale of the disaster.

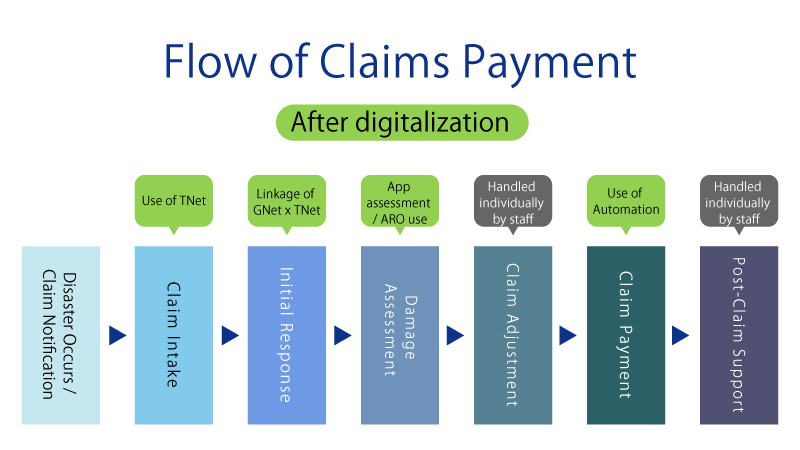

A new, centralized system for information

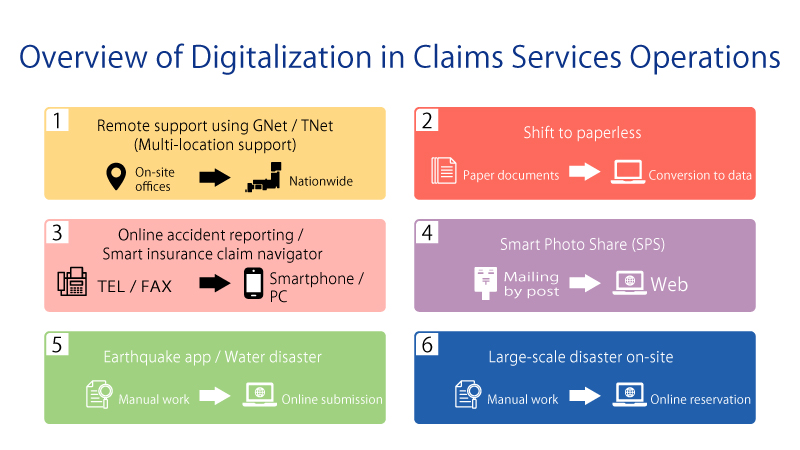

1. Diverse intake channels

The first area we addressed was the revamp of the claims intake process; the entry point to the entire workflow. We added online intake in addition to our conventional telephone and fax services. We designed our system to be easy to use not only on PCs but also on smartphones, enabling customers to complete procedures anytime, anywhere.

Additionally, TNet, the operational system for insurance agencies, was augmented with an intake function. By offering various intake methods, we ensured more reliable connectivity even during large-scale disasters, leading to greater peace of mind for our customers.

2. Introducing the GNet core system

GNet is an internal system for centralized management of accident response information. Accident information received by an agency is automatically imported into GNet through the aforementioned TNet. The process enables real-time company-wide sharing of initial response details, eliminating redundant communications such as having to repeat explanations or ask repeat questions to customers.

3. Multi-location response centers

We made great strides toward paperless operations, with a wide host of benefits beyond wasting less paper. All intake details and customer information are now stored as data within the system, enabling immediate access from locations nationwide. We were able to establish a multi-location system that enables support based on the same information as the field, even from remote sites outside of disaster-affected areas.

The transition marked a major shift in our claims service. We went from a field-dependent model to one supported by a nationwide, distributed framework. With nationwide offices able to back up operations, responses became faster and the workload at affected locations has been reduced, freeing up time for local representatives to focus on responses that can only be provided on-site.

Furthermore, by centralizing information, we established a framework that enables real-time tracking of accident intake and other metrics, allowing for flexible and optimal staffing.

4. Automating administrative tasks

GNet introduced an automation feature for administrative tasks. For simple processes like verifying no documents are missing from submissions, we increasingly rely on such automation.

With the freed up time, employees can better focus on interactions that can only be handled by humans, establishing a real connection with customers when handling complex communications, or assisting customers who struggle with digital processes.

A framework to expedite damage assessment

It is not only the information management system that has evolved. In striving to enable swift responses, we also developed new apps and systems for damage assessment, which is indispensable for claims payment.

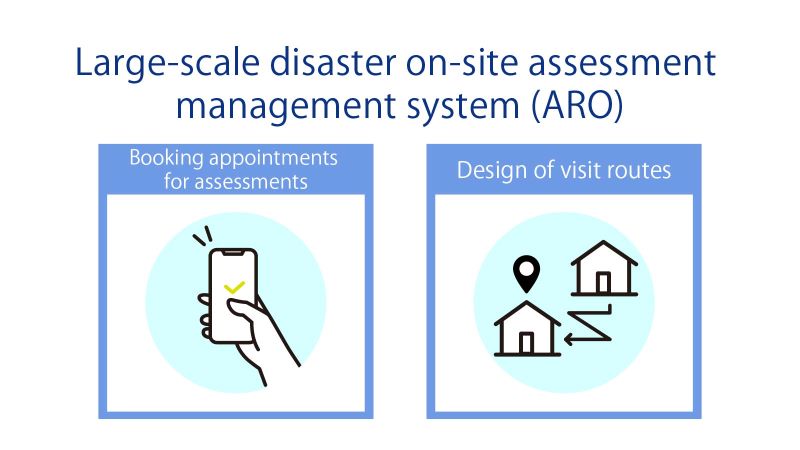

ARO, an information organizer for damage assessment

One of these was the large-scale disaster on-site assessment management system (ARO)*.

*An abbreviation of Appointment & Route Optimizer

ARO accelerates the process of scheduling on-site damage assessments and designing visit routes.

The ARO system not only enables appointment management for customer damage assessments but also allows customers to book their preferred assessment date and time via a dedicated link. The interface is familiar, similar to that of train or hotel reservation sites.

Furthermore, to efficiently visit multiple properties on the same day, the system also features AI that assigns properties to visit and proposes visit routes based on factors such as the number of members at the assessment site. In large-scale disasters, conducting numerous assessments within a short time frame is essential. This system helps establish a framework that optimizes response capabilities, even with limited staff.

ARO is also linked with the previously mentioned automation. For customers requiring on-site damage assessments, the system seamlessly connects intake to assessment: for example, automatically sending an ARO appointment URL for on-site visits.

Earthquake app to speed up assessment reporting

Conventional on-site damage assessments involved manually creating paper reports based on findings. This earthquake app, however, allows users to record the extent of damage using mobile devices and photograph damaged areas directly from within the app.

With paper reports, the adjuster had to return to the office once before handing the documents over to the person in charge of subsequent processes. It is now possible, however, to create and submit reports using the earthquake app at the assessment site or during transit, without returning to the office. Such initiatives have expedited claims payment.

From disaster occurrence to post-disaster response

We accomplished a fundamental revamp of the enterprise systems and automation of damage assessment management. These changes dramatically accelerated the process from accident intake to claims payment.

Prompt delivery of insurance claims provides a vital foundation for supporting the early reconstruction of disaster-stricken areas. We will continue to flexibly adopt new technologies and pursue the provision of faster, higher-quality services.

A Claims Service Framework for Nationwide Support

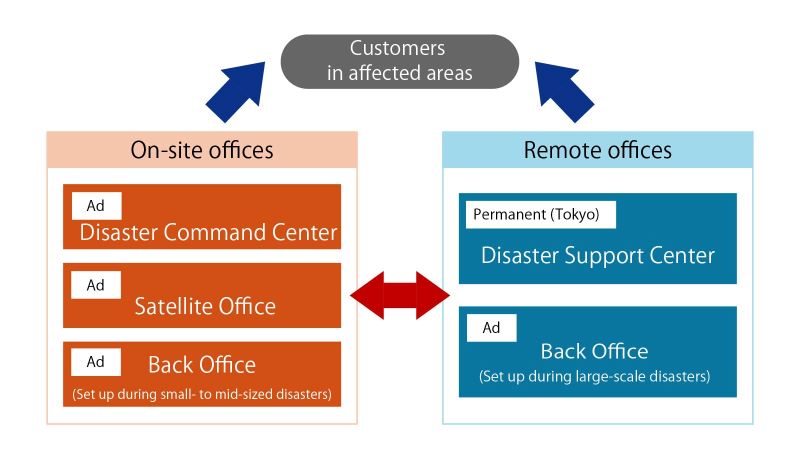

Beyond evolving the system, we also strengthened our internal structure within the Claims Service Division for large-scale disasters, to enable more rapid responses.

In the event of a disaster, claims services are delivered through coordination between on-site offices in the affected area and remote offices that are able to provide support.

Meanwhile, in remote locations, the permanent Disaster Support Center (Tokyo) handles tasks such as scheduling on-site assessments, digitizing documents, verifying reports, and conducting pre-payment screening, thereby reducing the workload of on-site staff. In the event of a large-scale disaster, a back office is also set up in remote locations to handle administrative tasks.

On-site teams concentrate on tasks that can only be performed locally, while other operations are supported remotely. Such a structure enables swift payments during large-scale disasters.

Digitalization Enabling Claims Payments

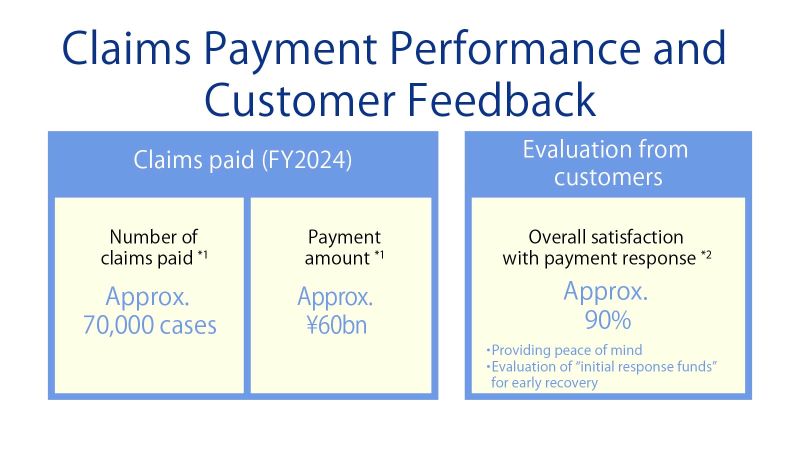

Our initiatives to introduce new tools, improve our internal structure, and pay faster and more reliable claims are steadily yielding tangible results. The number of claims paid in fiscal 2024 reached approximately 70,000, with the total payment reaching approximately 60 billion yen *1. Additionally, overall satisfaction with payments stands at approximately 90% *2.

-

*1Number of claims paid and payment amount for seven major disasters including the Hyogo Earthquake, Typhoon No. 10, and the Hyuga-nada Earthquake

-

*2Recent results of a questionnaire for policyholders of automobile and fire insurance regarding claim payments during disasters (February–July 2025)

Toward Further Evolution

Strengthening the response to large-scale disasters is an ongoing priority. To be there for our customers in times of need and contribute to a disaster-resilient society, we will continue to deepen our expertise in areas only humans can handle while automating what we can through digital and AI solutions.

With claims payments at the core, we will work toward achieving a disaster-resilient society through end-to-end support, from mitigation before disasters strike to rapid recovery and better reconstruction after they do.