The Group is committed to ERM*1 as the management platform for promoting its Mid-term Business Plan. Specifically, we will be constantly aware of the relationship between “risk,” “capital” and “profit,” and by realizing “capital adequacy” and “high profitability” in relation to risk, we will strive to achieve sustainable growth of corporate value.

*1Enterprise Risk Management

The risks surrounding Tokio Marine Group are becoming more diversified and complex due to global business development and changes in the business environment. In addition,in today’s uncertain and rapidly changing political,economic, and social climate, we must constantly watch for the emergence of new risks and take appropriate action. From this point of view, we are not limited to conventional risk management for the purpose of risk mitigation and avoidance, but are comprehensively assessing risk in qualitative and quantitative ways.

In addition, we are continuing our efforts to further strengthen the ERM structure. For instance, we are enhancing risk assessments to include risks that are difficult to quantify, such as cyber risks, and improving natural disaster risk management, including a review of our reinsurance schemes.

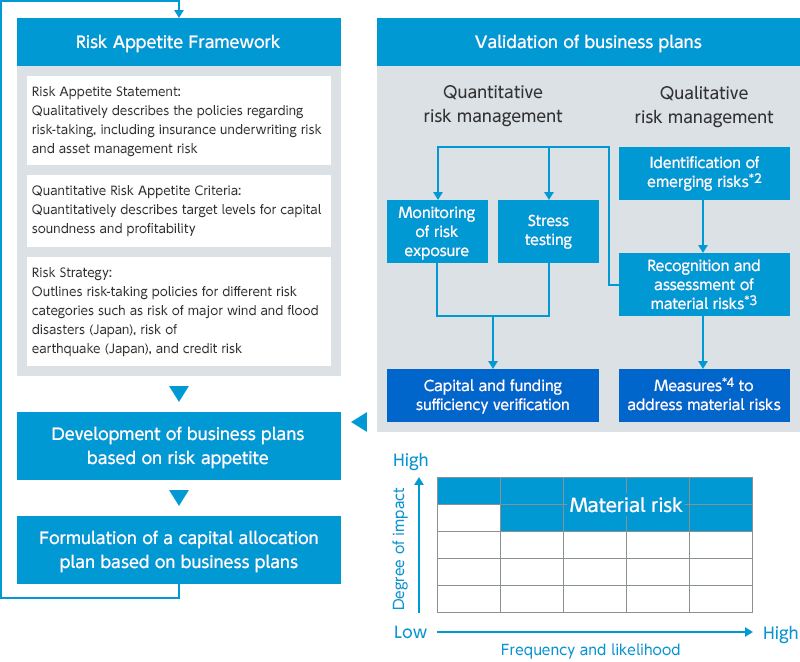

ERM Cycle

*2Emerging risks are new risks that arise due to changes in the environment or other factors, encompassing those that were not traditionally recognized as risks and those that have increased markedly in severity. Specifically, these risks are identified through internal discussions, considering results from subsidiary assessments and information from external sources.

*3Material risks refer to risks that could have a substantial impact on financial soundness, business continuity, and other critical aspects. Specifically, we focus on emerging risks as well as material risks from the previous business year within the Group. We assess the impact (evaluating economic, business continuity, and reputational impacts) and consider the frequency and likelihood to identify the most significant factors. We specify these risks using the following 5×5 matrix.

*4For material risks, we formulate response measures (Plan), implement these measures (Do), assess the outcomes (Check), and make improvements (Act).

(1) Qualitative Risk Management

In qualitative risk management, all risks, including risks that emerge due to changes in the environment, are identified and reported to management, while risks to the Group are discussed at the management level as needed.

Risks identified in this manner are evaluated not only in terms of the economic loss or frequency of occurrence but also in terms of business continuity and reputation. Risks that have a large impact on the financial soundness and business continuity of the Group or of individual Group companies are identified as “material risks.” For identified material risks, we assess the sufficiency of capital through the quantitative risk management process described below, draw up control measures before the risks emerge and countermeasures*5 to be taken if the risks do emerge,and conduct PDCA management.

*5Pre-emergence risk control measures include monitoring and risk management based on the market environment and regulatory trends, while post-emergence risk response measures include manuals (including business continuity plans) and mock drills.

Detection of Emerging Risks and the Process of Identifying Material Risks

Examples of Emerging Risks

Emerging risks/Scenarios

Examples of responses

(1) Progressive deterioration of public infrastructure and corporate facilities

Risk that insurance payouts will increase as growing deterioration of public infrastructure and corporate facilities leads to frequent major accidents

Response to economic impact

Appropriately assess risks and develop products that meet customer needs, while generating stable profits through risk-appropriate underwriting, risk diversification, and arranging reinsurance

With respect to (4) above, engage in research and analysis on the impacts of climate change

(2) Space risk

Risk that insurance payouts will increase due to widespread power grid failures caused by geomagnetic storms and frequent communication disruptions resulting from space weather and increased space debris

(3) Innovations in medicine and biotechnology

Risk that insurance payouts will increase due to innovations in cancer diagnosis and genetic diagnosis technologies

(4) Global warming (physical risks of climate change)

Risk that insurance payouts will increase due to intensifying environmental degradation and disasters caused by global warming

(5) Inadequate response to decarbonization (climate change transition risk)

Risk of a decline in value of invested companies that lag behind in transitioning to a decarbonized society, impacting the value of the Group’s assets

Risk that the Group’s efforts towards decarbonization are perceived as inadequate by society, damaging our reputation

Response to the impact on business continuity and reputation

Publicly disclose our fundamental approach to climate change,underwriting and investment policies, and the initiatives based on these, and exchange opinions with experts and advisors in the climate field

(6) Delayed response to stricter global focus on human rights

Risk that Tokio Marine Group’s efforts regarding respect for human rights are perceived as inadequate by society, damaging our reputation

Response to the impact on business continuity and reputation

Publicly disclose our fundamental approach to human rights, human rights basic policies, management structure for respect of human rights,guidelines for responsible procurement, and initiatives based on these,and exchange opinions with experts and advisors in the human rights field

Material Risks for Fiscal 2023

Emerging risks/Scenarios

Examples of responses

(1) Domestic or overseas economic crisis, chaos in financial and capital markets

The value of the Group’s assets may fall substantially due to a global economic crisis on the magnitude of the 2008 global financial crisis occurs, or turmoil in financial and capital markets caused by geopolitical risk.

Response to economic impact

Investigate the impact on the market due to geopolitical risks

Control exposure through credit risk aggregation and management

Conduct stress tests to confirm capital adequacy and funding liquidity

Establish action plans for financial crises and interest rate increase risks

(2) Loss of confidence in JGBs

The value of the Group’s assets may fall substantially as Japanese government bonds plummet in value due to a decline in the government’s creditworthiness or the emergence of hyperinflation.

(3) Major earthquakes

A major earthquake beneath Tokyo or along the Nankai Trough may lead to significant human and material losses, causing widespread disruptions to social and economic activities, including those of the Group, resulting in large insurance payouts.

Response to economic impact

Appropriately assess risks, including risk aggregation,and develop products that meet customer needs, while generating stable profits through risk-appropriate underwriting, risk diversification, and arranging reinsurance

With respect to (3), (4), and (6) above, conduct stress tests to confirm capital adequacy and funding liquidity

Response to the impact on business continuity and reputation

Establish crisis management systems and business continuity plans, and verify their effectiveness through emergency drills

With respect to (7) above, develop cybersecurity measures, and verify their effectiveness through emergency drills

(4) Major wind and flooding disasters (including physical risks of climate change)

Major typhoons or torrential rains may cause extensive physical damage, leading to significant disruptions in social and economic activities, including those of the Group,resulting in large insurance payouts.

(5) Volcanic eruptions

The eruption of Mount Fuji or similar volcanic activities could result in widespread physical damage due to volcanic ash and other effects, leading to significant disruptions in social and economic activities, including those of the Group, resulting in large insurance payouts.

(6) Pandemics

The widespread outbreak of a new infectious disease could result in significant insurance payouts.

(7) Cyber risk

A cyberattack targeting many Group customers or supply chains may lead to significant insurance payouts.

A cyberattack targeting the Group’s systems may result in the leakage of sensitive information and disruptions to business operations.

(8) Inflation

Due to soaring raw material costs and rapid increases in global prices, insurance payout costs rise, resulting in diminished underwriting profits from the inability to revise products in line with risks or secure reinsurance.

Response to economic impact

Analyze the impact of inflation on insurance products and undertake product revisions and underwriting commensurate with risk

(9) Disruptive innovation

Innovations that drastically reshape industry structures through digital transformation and innovative new entrants may erode the Group’s competitive advantage and lead to significant reductions in premium income and profits.

Response to economic impact

Ensure the competitive advantage of our insurance business by implementing basic strategies and executing projects for digital transformation

Expand into new businesses, primarily in areas closely aligned with our insurance operations

(10) Continued mutation of COVID-19 virus

The continued mutation and sustained spread of COVID-19 may lead to disruptions in business activities.

Response to the impact on business continuity and reputation

Establish crisis management systems and business continuity plans, and verify their effectiveness through emergency drills (Response to economic impact is detailed in (1) above)

(11) Geopolitical risk

Escalation of tensions between nations into military conflicts could lead to extensive human and material damages, leading to significant disruptions in social and economic activities, including those of the Group.

(12) Conduct risk

Deviation between industry and corporate practices and societal norms could lead to the perception that the initiatives of the Tokio Marine Group are inadequate by society,damaging our reputation.

Response to the impact on business continuity and reputation

Conduct surveys on employee awareness and behavior, and enhance the efforts of the Group by compiling and sharing best practices

(13) Violation of laws and regulations

Non-compliance with regulations concerning personal data protection, anti-money laundering, and the reinforcement of economic sanctions related to the US-China tensions and the Ukraine conflict may result in the imposition of fines and penalties and harm the Group’s reputation.

Response to the impact on business continuity and reputation

Monitor domestic and international social environments, trends in government agencies, and changes in regulatory requirements, and take necessary measures accordingly

(2) Quantitative Risk Management

In quantitative risk management, the Company measures risk amounts and conducts stress tests using risk models based on the latest knowledge available, verifying from multiple perspectives that its capital is sufficient relative to the risks it holds, with the aim of maintaining its credit ratings and preventing bankruptcy.

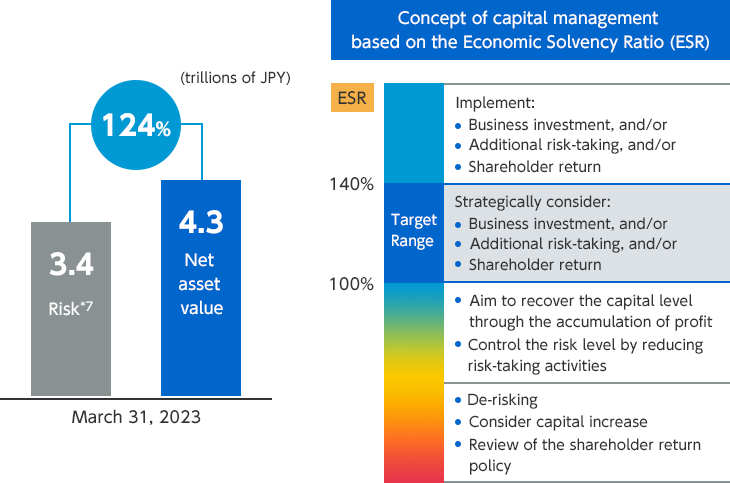

Specifically, the Company quantifies potential risks using a statistical metric called “Value at Risk (VaR)” on a 99.95% confidence level, which corresponds to an AA credit rating, and verifies its capital adequacy based on the Economic Solvency Ratio (ESR) arrived at by dividing net asset value*6 by risk capital. A 99.95% VaR is equivalent to the damage caused by an occurrence of a risk that happens once in 2,000 years. Although many insurance companies around the world use 99.5% VaR (once in 200 years), Tokio Marine Group uses a much more stringent standard to evaluate risk capital.

The target range of the Group’s ESR is 100%‒140%, and as of March 31, 2023, the Group’s ESR was 124%, confirming that the Group is adequately capitalized.

We also conduct stress tests based on scenarios involving significant economic losses from material risks such as domestic and international economic crises, disruptions in financial and capital markets, loss of confidence in Japanese government bonds, major earthquakes, major wind and water-related disasters, and widespread outbreaks of new viruses. We also assess scenarios where multiple critical risks materialize simultaneously. Through these stress tests,we confirm separately that there are no issues regarding capital adequacy and liquidity.

*6Calculated by adding the value of catastrophe loss reserves, deducting for goodwill, and making other adjustments to consolidated net assets on a financial accounting basis.

Status of the Economic Solvency Ratio (ESR)

*7Amount of risk calculated by a model using 99.95% VaR (AA-rated basis)

![[Emerging Risks] New risks that emerge due to changes in the environment or other factors, and that have not been previously recognized as risks, or risks that have increased markedly in severity. Potential emerging risks: Emerging risks for major Group companies. New emerging risks identified by the CRO or risk management department. Emerging risks identified in the previous fiscal year. Risk information from external sources. 1 Screening → Emerging risks → [Material Risks] Risks that have a significant impact on financial soundness, business continuity, etc. Potential material risks: Material risks of the Group in the previous year. High-impact risks among the emerging risks. 2 Identification by matrix evaluation → Material risks → PDCA for material risks](/en/ir/financial/images/img_risk_02.png)